Carriers running out of time to bring down capacity

Carriers are expected to announce a host of blank sailings to counteract supply-side growth

Absent any serious demand growth, carriers are expected to announce a host of blank sailings to counteract supply-side growth, according to the latest update from Sea-Intelligence.

"In week 42, we looked at the post-Golden week capacity deployment on Transpacific and Asia-Europe and saw substantial overcapacity on both trades. Four weeks on, hardly any new blank sailings have been announced, and capacity growth for the remainder of 2023 is still quite excessive."

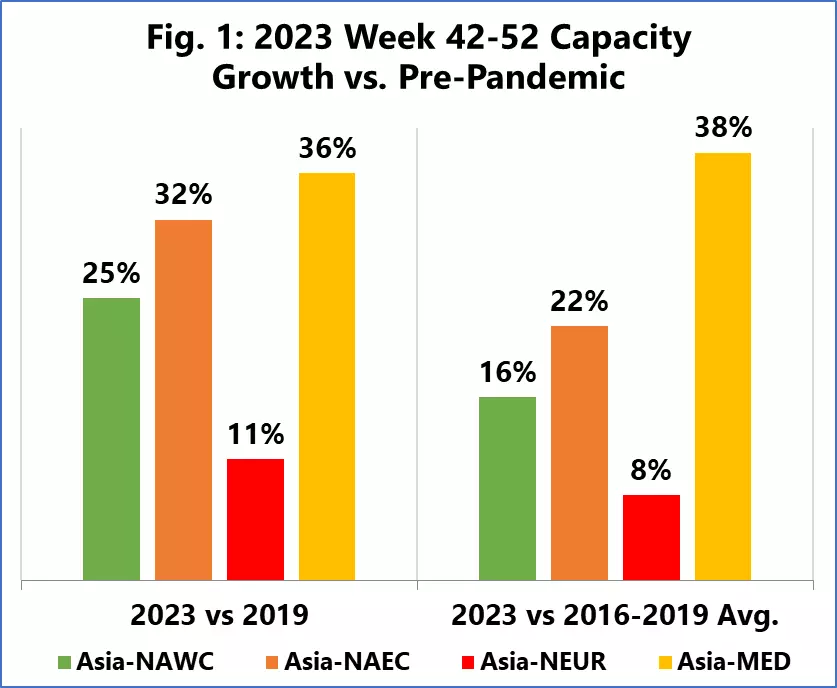

Figure 1 shows a summary of these growth figures, based on the latest vessel deployments (as of Week 46, 2023). "These figures are for the last 10 weeks of 2023 (Weeks 42-52), net of the growth in 2019, as well as net of the average growth across 2016-2019. What this means is that Figure 1 does not show what the actual growth looks like but by how much higher it is compared to the pre-pandemic years."

Alan Murphy, CEO, Sea-Intelligence says: "Depending on whether we compare the capacity growth post-Golden Week 2023 to the same time in 2019 or to the average growth of 2016-2019, Asia-North America West Coast is up by 16-25 percent, Asia-North America East Coast by 22-32 percent, Asia-North Europe by 8-11 percent, and Asia-Mediterranean by 36-38 percent. These are all unsustainable capacity growth figures."

With six weeks to go to the end of 2023, there are pretty much two ways in which this plays out, the update added. "Either the carriers announce a massive blank sailings programme between now and the end of the year, which will reduce capacity but will not go down well with the shippers as it will leave them scrambling to manage these sudden supply-side disruptions. Or the carriers ride this wave of high capacity injection and the likely downwards pressure on freight rates into the new year, and compensate for it during Chinese New Year."