Long Beach handled lesser containers in Oct, freight rates steady

Port of Long Beach handled 789,716 TEUs in October 2021, down 2.1 percent from October 2020 but still the second-busiest October on record.

November 12, 2021: Port of Long Beach handled 789,716 TEUs in October 2021, down 2.1 percent from October 2020 but still the second-busiest October on record.

While imports declined over four percent to 385,000 TEUs, exports increased 6.6 percent to 122,214 TEUs. Empty containers moved through the port declined 2.4 percent to 282,502 TEUs.

“Every sector of the supply chain has reached capacity and it is time for all of us to step up and get these goods delivered,” said Mario Cordero, executive director, Port of Long. “In Long Beach, we are trying to add capacity by searching for vacant land to store containers, expanding the hours of operation at terminals, and implementing a fee that will incentivise ocean carriers to pull their containers out of the port as soon as possible.”

The port moved 7.9 million TEUs during the first 10 months of 2021, up 21% from the same period in 2020.

Long Beach and the Los Angeles port began assessing a congestion dwell fee from November 1 of $100/day per container for cargoes that remain on a terminal for more than eight days. The fees will increase by $100/d, and it will be $300/container on day 10 and $1,500 on day 13.

Data published by the Los Angeles port show containers dropped 16 percent to 73,691 at the end of November 10 from 87,485 on November 1.

In an advisory to customers on November 11, Danish shipping firm A.P. Moller-Maersk said the dwell fees charged to carriers would be passed along to shippers as an Emergency Government Port Storage Charge, S&P Platts said in an update.

While containers have started moving, congestion across LA/LB and other U.S. ports continue. As many as 78 carriers continue to be anchored around LA/LB ports.

(Source: Sea Explorer)

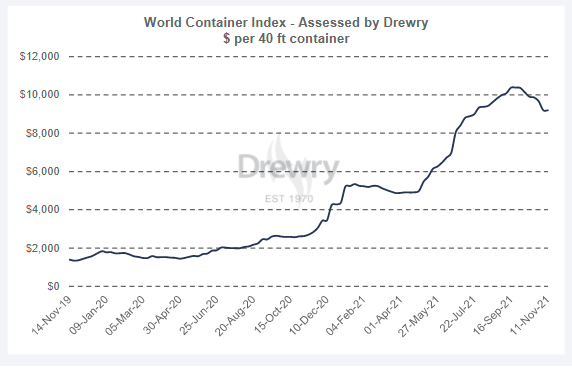

Freight rates steady

Drewry’s composite World Container index was steady at $9,192.50 per 40ft container this week.

Though the composite index was steady, it remains 250 percent higher than a year ago.

Drewry is expecting rates to remain steady in the coming week.

Container shipping industry expert Lars Jensen said he would be hesitant in concluding that the current decline signals a coming large decline and reversal to normal rate levels. "It seems to imply that the worst pressure on the Transpacific might have been alleviated, but the global capacity shortage persists as we cannot see a similar impact on Asia-Europe, Europe-North America or Europe to South America in the FBX data."