African airlines report strong growth in cargo volumes

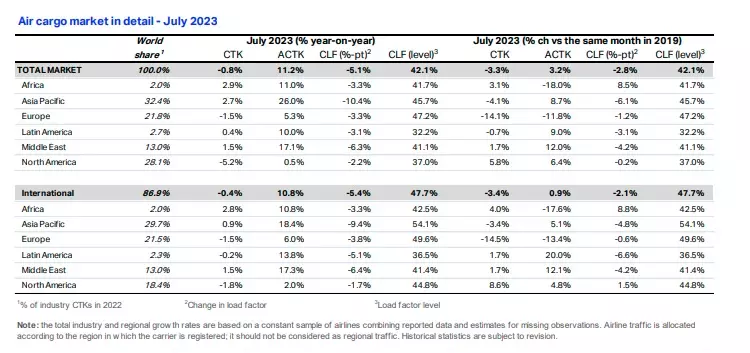

Global air cargo demand in July 2023 was marginally (0.8%) lower YoY even as capacity increased over 11%

Listen to this Article

African airlines had the strongest performance in July 2023 with a 2.9 percent increase in cargo volumes compared to July 2022, according to the latest update from the International Air Transport Association (IATA).

"Notably, Africa–Asia routes experienced significant cargo demand growth (10.3 percent). Capacity was 11 percent above July 2022 levels," the update added.

Global air cargo demand was marginally (0.8 percent) below the previous year’s levels but is an improvement on recent months’ performance that is particularly significant given declines in global trade volumes and rising concerns over China’s economy.

Global demand, measured in cargo tonne-kilometers (CTKs), was a significant improvement over the previous month’s performance (-3.4 percent). "The global air cargo industry registered 20.7 billion CTKs in July, extending its steady improvement since February while remaining 3.3 percent lower than their pre-pandemic level in 2019. The improved annual growth rate in global CTKs is also a result of growth stemming from a lower 2022 baseline."

Capacity, measured in available cargo tonne-kilometers (ACTKs), was up 11.2 percent compared to July 2022 (eight percent for international operations). "The strong uptick in ACTKs reflects the growth in belly capacity (29.3 percent year-on-year) due to the summer season."

Willie Walsh, Director General, IATA says: “Compared to July 2022, demand for air cargo was basically flat. Considering we were 3.4 percent below 2022 levels in June, that’s a significant improvement. And it continues a trend of strengthening demand that began in February. How this trend will evolve in the coming months will be something to watch carefully. Many fundamental drivers of air cargo demand such as trade volumes and export orders remain weak or are deteriorating. There are growing concerns over how China’s economy is developing. At the same time, we are seeing shorter delivery times, which is normally a sign of increasing economic activity. Amid these mixed signals, strengthening demand gives us good reason to be cautiously optimistic."

July regional performance

Asia-Pacific airlines saw cargo volumes increase by 2.7 percent in July 2023 compared to the same month in 2022. This was a significant improvement in performance compared to June (-3.3 percent). Carriers in the region benefited from growth on three major trade lanes: Europe-Asia (3.2 percent YoY growth), Middle East-Asia (up from 1.8 percent in June to 6.6 percent in July) and Africa-Asia (returning to double-digit growth of 10.3 percent YoY from -4.8 percent in June). Additionally, the within-Asia trade lane also performed considerably better in July with an annual decline of international CTKs at 7.5 percent compared with the double-digit decreases observed since September 2022. Available capacity in the region increased by 26 percent compared to July 2022 as more belly capacity came online from the passenger side of the business.

Asia-Pacific airlines saw cargo volumes increase by 2.7 percent in July 2023 compared to the same month in 2022. This was a significant improvement in performance compared to June (-3.3 percent). Carriers in the region benefited from growth on three major trade lanes: Europe-Asia (3.2 percent YoY growth), Middle East-Asia (up from 1.8 percent in June to 6.6 percent in July) and Africa-Asia (returning to double-digit growth of 10.3 percent YoY from -4.8 percent in June). Additionally, the within-Asia trade lane also performed considerably better in July with an annual decline of international CTKs at 7.5 percent compared with the double-digit decreases observed since September 2022. Available capacity in the region increased by 26 percent compared to July 2022 as more belly capacity came online from the passenger side of the business.

North American carriers posted the weakest performance of all regions with a 5.2 percent decrease in cargo volumes in July 2023 compared to the same month in 2022, marking the fifth consecutive month in which the region had the weakest performance. It was, however, a slight improvement compared to June (-5.9 percent). The transatlantic route between North America and Europe saw traffic declining by 4.3 percent in July, 1.2 percentage points worse than the previous month. Capacity increased 0.5 percent compared to July 2022.

European carriers saw their air cargo volumes decline by 1.5 percent in July compared to the same month in 2022. This was an improvement in performance versus June (-3.2 percent). Volumes were affected due to the Europe–North America performance and contractions in the Middle East-Europe (-1.2 percent) and the within-Europe (-5.1 percent) markets. Capacity increased 5.3 percent in July 2023 compared to July 2022.

Middle Eastern carriers experienced a 1.5 percent year-on-year increase in cargo volumes in July 2023. This was also an improvement to the previous month’s performance (0.6 percent). The demand on Middle East–Asia routes has been trending upward in the past two months. Capacity increased 17.1 percent compared to July 2022.

Latin American carriers posted a 0.4 percent increase in cargo volumes compared to July 2022. This was a drop in performance compared to the previous month (2.2 percent). Capacity in July was up 10 percent compared to the same month in 2022.

Next Story